Expedia And Hilton: A Pair Commerce For The Streamlined Journey Sector

400tmax/iStock Unreleased through Getty Photographs

On January 2, Looking for Alpha printed my pair commerce advice to go lengthy shares of LVMH and quick shares of Ross Shops (ROST). To this point, LVMH is up 15.1% and ROST down 0.77%, yielding a tidy web revenue 8% for the market impartial commerce up to now. I imagine there may be loads of room to run, as the elemental story continues to play out.

For client discretionary spending as a complete, Macy’s (M) is the proverbial canary within the coal mine. On January 6, Macy’s issued weak steerage and a somber description of the present state of the US client. Any hope for Macy’s to be written off an as anomaly was eradicated by Nordstrom’s (JWN) the next week, when the Firm reduce earnings estimates and in addition warned of tightening client spending habits.

Costs stay inflated in a US financial system concurrently topic to quantitative tightening by the Fed. Diminished client budgets dictate that 2023 and foreseeably past can be outlined by completely different spending patterns, and a complete lot much less consumption general in low-middle earnings households.

Frequent vacationers, be it for enterprise or leisure, will proceed to make use of rewards applications with their favourite landlords relatively than permitting middlemen journey brokers to earn mentioned rewards, after which some, as fee. Proprietor operators akin to Hilton (NYSE:HLT) and Marriott (MAR) face macro headwinds, but they’ve largely prosperous clientele whose loyalty quantities to nearly subscription-like income streams. Moreover, costs supplied immediately by way of proprietors’ web sites now match these supplied by broadly used on-line journey brokers. In early years, journey web sites supplied discounted charges on particular blocks of rooms whereas manufacturers like Hilton targeted on prospects much less involved with value or on the lookout for luxurious facilities and repair. Shoppers have been educated in an nearly Pavlovian method to keep away from direct bookings in favor of web sites like Priceline.com, now Reserving.com, with a view to get the perfect deal. The identify change is sort of telling in that reductions are now not a part of the equation.

Extra sporadic vacationers, primarily these seeking to evaluate all charges with minimal requirements, will largely proceed to make use of handy web sites that simply evaluate completely different choices, however how a lot will these shoppers truly journey and the way a lot will they spend going ahead? 2022 was a novel aberrational boon for journey and leisure, outlined by momentary pent-up demand from COVID induced shutdowns.

It’s fairly clear that if the present financial surroundings persists, by which margins are persistently being squeezed, on-line journey brokers will successfully disappear in time as did their strip mall predecessors. To make a Seinfeld analogy, the pool by which Expedia, Reserving, TripAdvisor and the like function has turn into frigid. Their high strains are due for, as George Costanza would say, “important shrinkage.”

Consolidation can be inevitable amongst the net journey brokers, with Expedia and Reserving the one probably survivors. Earlier than that happens, every inventory will endure a brutal revaluation primarily based on a client panorama that leaves much less meat on the bone for all companies, particularly people who depend upon low-to-middle earnings discretionary spending.

Solely in latest days, Reserving Holdings (BKNG), the pronounced worldwide chief on this sector, trades at an earnings low cost to second fiddle Expedia (NASDAQ:EXPE). McDonald’s (MCD) trades at a premium to Burger King (QSR), JPMorgan (JPM) trades at a premium to Citi (C) and Wells Fargo (WFC), Nvidia (NVDA) trades at a premium to Superior Micro (AMD). There may be at all times a greatest in breed and in all of the above examples, in addition to the case of BKNG vs EXPE, there isn’t any debate. BKNG operates with EBITDA margins just lately simply above 30% and pre-COVID usually round 40%, whereas EXPE has been extra constantly round 20%. EXPE now garners the next P/E, in extra of 39x, with the next debt to fairness ratio as well!

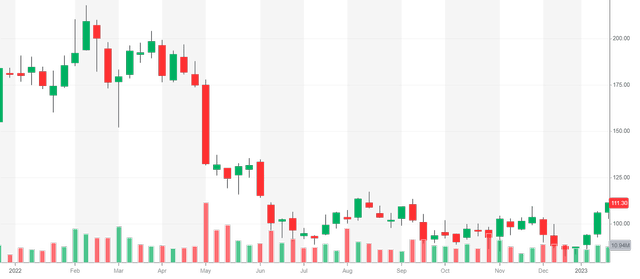

On a technical foundation, the EXPE chart is an absolute catastrophe. The inventory didn’t backside with the general market in August, it continued to say no within the following months regardless of quick curiosity reaching multi yr lows. With shares within the $80s, quick curiosity within the inventory shrank to 2% in late 2022 from over 10% in 2021. This strongly signifies that good cash was closely quick with shares over $150 and lined profitably below $100.

Expedia bubble bursts (Yahoo Finance)

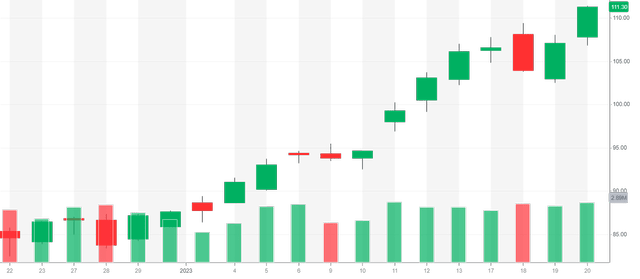

Since bottoming Dec 22, shares of EXPE are up a whopping 35%. In the identical interval, BKNG shares are up a comparatively paltry 16%, which totally explains the valuation discrepancy. Notably, proven beneath, shares of EXPE gapped up from $94.64 on the shut on 1/10/23 to $97.98 on the open on 1/11/23 and have not regarded again since. Over the past 2 years, each hole on the day by day chart has stuffed, suggesting an imminent return to $94.64 or beneath. Quick curiosity rapidly climbed again to 4% after the primary buying and selling week of 2023 and sure sits a lot greater as shares went up in unsustainably parabolic trend following the aforementioned hole up.

Hole up in EXPE (Yahoo Finance)

Expedia, like Ross Shops, noticed peak demand in 2022. The Firm is just not positioned for development in 2023, regardless of a valuation that claims in any other case. With multiples cratering in conventional development sectors akin to tech, it appears unsustainable that journey brokers will proceed to garner such large multiples.

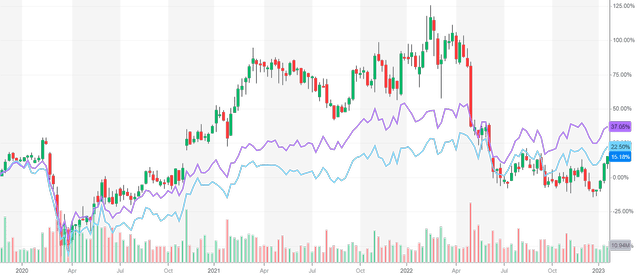

Clearly, my greater conviction play right here is shorting EXPE, nevertheless managing beta is important to any portfolio and the inventory is sort of risky. A pair commerce retains the bear in me balanced and may generate alpha with out leverage, no matter general market path. There are a number of causes I select Hilton over Marriott for the lengthy half of this commerce, regardless of it being dearer primarily based on most metrics. Marriott, like Expedia, accrued extra debt within the third quarter of 2022 whereas Hilton decreased debt. Hilton properties cater to a considerably extra prosperous clientele as a complete. Moreover, the inventory has confirmed relative power in recent times, as proven within the chart beneath.

EXPE vs HLT (purple) vs MAR (blue) (Yahoo Finance)

Some enterprise fashions have elementary endurance, others are merely designed to seize excesses when the water is sweet and heat. Hilton constitutes the previous, Expedia the latter. Traders on the lookout for extra certainty earlier than shorting the risky inventory can wait till EXPE experiences earnings February 9. I am going to in all probability provoke a brief place earlier than then, because the response will probably be unfavorable if the Firm experiences a disappointing money burn of $2B because it did the quarter prior.

Quick Expedia, Lengthy Hilton.

Source link