Disney’s Theme Parks May Not Be So Magical Anymore (NYSE:DIS)

CatLane

We’ve got beforehand coated Walt Disney Firm (NYSE:DIS) here in November 2022. After the poor FQ4’22 outcomes, notably the unprofitable D2C streaming, Bob Chapek was changed by Bob Iger, who got here out of retirement to function an interim CEO for the following two years. Given the large shift in client habits post-pandemic, its theatrical releases have been underwhelming as effectively, considerably worsened by the lowered promoting income from ESPN and Hulu.

For this text, we’ll deal with DIS’s theme park efficiency so far, which has been struggling to return to pre-pandemic attendance ranges. Notably, its rival, Common Studios (CMCSA), seems to be extra in style lately, displacing the previous’s reputation in comparison with pre-pandemic ranges. Mixed with the overly inflated park costs, rising dissatisfaction amongst parkgoers, and the Florida Particular district overhang, it’s unsurprising that the inventory has considerably retraced within the previous few months.

The Theme Park Funding Thesis Is Shaky

Within the newest fiscal yr, DIS reported glorious domestic theme park sales of $20.13B with working incomes of $7.9B, and working margins of 26.4%, accounting for twenty-four.3% of its revenues then. However, the worldwide section continues to underperform, attributed to China’s Zero Covid Coverage impacting its theme parks in Hong Kong and Shanghai then. Nonetheless, issues might enhance from Q2’23 onwards, as soon as the Chinese New Year festivities are concluded and Covid-19 infections peak.

Within the meantime, DIS’ linear community section has been glorious, delivering revenues of $28.34B, working incomes of $8.51B, and working margins of 30% in FY2022. However, its D2C section has underperformed, with revenues of $19.55B, working incomes of -$4.01B, and working margins of -20.5% on the similar time.

It is very important set up these numbers as DIS theme parks stay the spine of its operations, particularly since they’re worthwhile and stay in excessive demand. Whereas it’s comprehensible that Bob Chapek has continued to lift park costs to maintain up with rising inflationary pressures, it seems that the hikes have been overly aggressive.

DIS’ admission costs elevated by 73% YoY to $189 from 2023 onwards (relying on the dates chosen), with parkgoers equally charged as much as $211 per person for after-hours access to Christmas parades and fireworks. It is very important spotlight that the latter was not individually charged pre-pandemic. The beforehand free FastPass ride reservation system has additionally been changed with a Genie+ at $29 per particular person/day (precedence line-skipping entry) and particular person attraction alternatives for one more $25 per particular person/experience/day (categorical entry).

Based mostly on the average US household size of 4 persons (rounded up from 3.14) and the standard four-day trip (together with park tickets and Genie+ solely), a median household must spend roughly $2.72K now, in comparison with $1.3K in 2019. That may be a great progress of 109.2%, considerably worsened by the slower wage increases of 11.9% on the similar time. Whereas we’re assured about DIS’ pricing energy, it’s unsure if client demand will stay strong by way of the unsure macroeconomic outlook and extended curiosity ache by way of 2024.

The TripAdvisor ratings for DIS’ Walt Disney World Resort in Orlando stay glorious at 4.5/5 on the time of writing. Nonetheless, critiques for the previous six months have been alarmingly destructive. Thirty-eight of fifty newest reviewers have given lower than 2/5 rankings, with frequent complaints of being overpriced, overcrowded, queues of greater than 120 minutes every, lowered staffing/ solid members, and sophisticated reserving methods, amongst others. Whereas it stays to be seen if the expertise is analogous throughout the board, it’s a big purple flag when many have pledged to chorus from returning afterward.

The DIS administration has lately attempted to make amends for the revenue-based strikes. Nonetheless, it stays to be seen if the Disney Magic expertise might be restored post-Chapek-ousting. Moreover, the latest data released in October 2022 reveals that parkgoers are more and more selecting Common Studios over Disney World Parks, with three of the latter dropping out of the highest 4 spots since 2019.

Notably, DIS’ theme parks have struggled to hit pre-pandemic attendance ranges, with the Magic Kingdom solely reporting a 60.5% restoration then, towards Common Studios Florida’s spectacular variety of 82.2% and Common Islands of Journey of 87.4%. Whereas a number of the shortfalls could also be attributed to the lowered worldwide journey, it seems that Common Studios doesn’t undergo from the identical malaise.

It stays to be seen how DIS’ theme parks have carried out in 2022, because the administration doesn’t report customer numbers. Nonetheless, early stories are usually not promising, suggesting that the attendance for Magic Kingdom remained beneath -36.6% of its designed capacity of 90K, with the remaining underperforming at a median of -51.4%.

So, Is DIS Inventory A Purchase, Promote, Or Maintain?

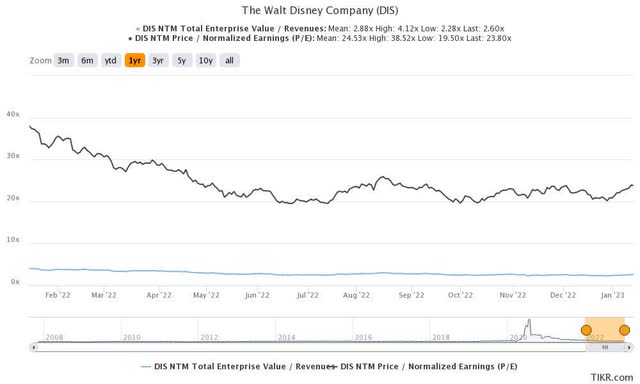

DIS 1Y EV/Income and P/E Valuations

S&P Capital IQ

DIS is at the moment buying and selling at a NTM P/E of 23.80x, greater than its 3Y pre-pandemic imply of 18.04x, although decrease than its 1Y imply of 24.53x.

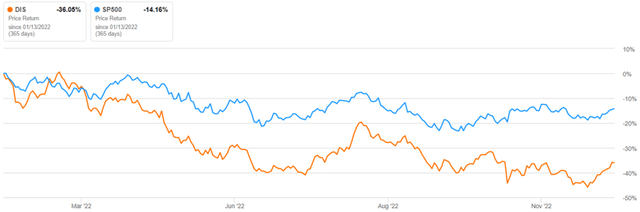

DIS 1Y Inventory Value

In search of Alpha

Based mostly on DIS’ projected FY2024 EPS of $5.43, we’re a average value goal of $129.23. These mirror the consensus goal of $120.09 as effectively, suggesting a 20.9% upside potential from present ranges. Then once more, we should spotlight that the inventory has notably declined by -46.5% by the top of December 2022, earlier than reasonably recovering by 18.2% prior to now two weeks.

A part of the headwinds are seemingly attributed to Bob Chapek’s ouster. In line with market analysts, the occasion was seemingly prompted by the unprofitable D2C section, operational losses, deceleration in wage progress, decline in market cap, and notably political controversy. Whereas some might have posited that Bathroom Iger’s return might probably set off an amicable decision with Florida lawmakers, we aren’t as optimistic. Bryan Griffin, the governor’s press secretary, has launched this assertion:

Governor DeSantis doesn’t make “U-turns.” The governor was proper to champion eradicating the extraordinary profit given to at least one firm by way of the Reedy Creek Enchancment District. We can have a good taking part in area for companies in Florida, and the state definitely owes no particular favors to at least one firm. Disney’s money owed is not going to fall on the taxpayers of Florida. A plan is within the works and might be launched quickly. (Source)

Due to this fact, we posit that the Florida lawmakers might select to dilute the present Reedy Creek board by appointing new state-approved members, thereby ending DIS’ self-governance in Florida. As well as, new development initiatives akin to resort or theme park expansions can also require native counties’ approval, triggering sophisticated approval/ submission processes.

The purple tape might subsequently dissuade DIS’ new infrastructure investments in Florida for the intermediate time period. Even Bob Iger himself has launched this assertion within the firm’s latest townhall:

I used to be sorry to see us dragged into that battle, and I do not know precisely what its ramifications are. The state of Florida has been vital to us for a very long time, and we have now been crucial to the state of Florida. (Financial Times)

Then once more, with DIS’ $1B in bond obligations and an current greater property tax charge in comparison with close by counties, these from the Happiest Place on Earth can also have some negotiating energy. Some analysts have optimistically posited that the brand new invoice might solely take away DIS’ rights to assemble a nuclear energy plant and airport in Reedy Creek, based mostly on the unique settlement in 1967.

For now, these are our speculations and issues will stay unclear for the following few months, till a decision is reached by June 2023 following approval from the Legislature by Could 2023. Consequently, it’s believable to imagine that the DIS inventory might stay risky, partly attributed to Bob Iger’s restructuring bills over the following few quarters.

Mixed with the unpromising early reports of Netflix’s (NFLX) ad-support tier, it stays to be seen if DIS’s providing will succeed. Due to this fact, it is perhaps higher to attend for its upcoming FQ1’23 earnings name on 08 February 2023, earlier than making a choice. Traders wanting so as to add might think about the $80s degree, if it ever comes once more, because of the improved margin of security.

Source link